The Thinking SME Bank: Part 1 of 12

The Reactive Banking Paradigm

Why Current SME Banking Models Fall Short

Reading time: 11 minutes

The Big Idea

Banks have invested billions in digital transformation, yet SME satisfaction with banking services continues declining. The reason isn't execution—it's architectural obsolescence. Most banks are optimizing Era 3 (digital reactive) while the market shifts to Era 4 (intelligent anticipatory). This chapter explores why we're facing not an execution problem, but a paradigm that no longer serves modern business velocity.

I. The System That Fails By Design

Banks have invested $340 billion globally in digital transformation over the past decade. Mobile apps are faster. Onboarding is paperless. Customer service is 24/7. Credit decisions take days instead of weeks.

Yet SME satisfaction with banking has declined 12% since 2019.

This isn't a paradox. It's a diagnosis.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ THE UNCOMFORTABLE TRUTH

Your digital transformation is failing. Not because of poor execution, insufficient budget, or weak talent. It's failing because you're optimizing an obsolete architecture.

Every dollar spent making reactive banking faster, prettier, or more efficient is a dollar that delays the inevitable reckoning with architectural obsolescence.

The harder truth: your board likely doesn't understand the difference between digital optimization and architectural transformation. And if you're reading this wondering whether to explain it to them, that hesitation is exactly why challengers will win.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

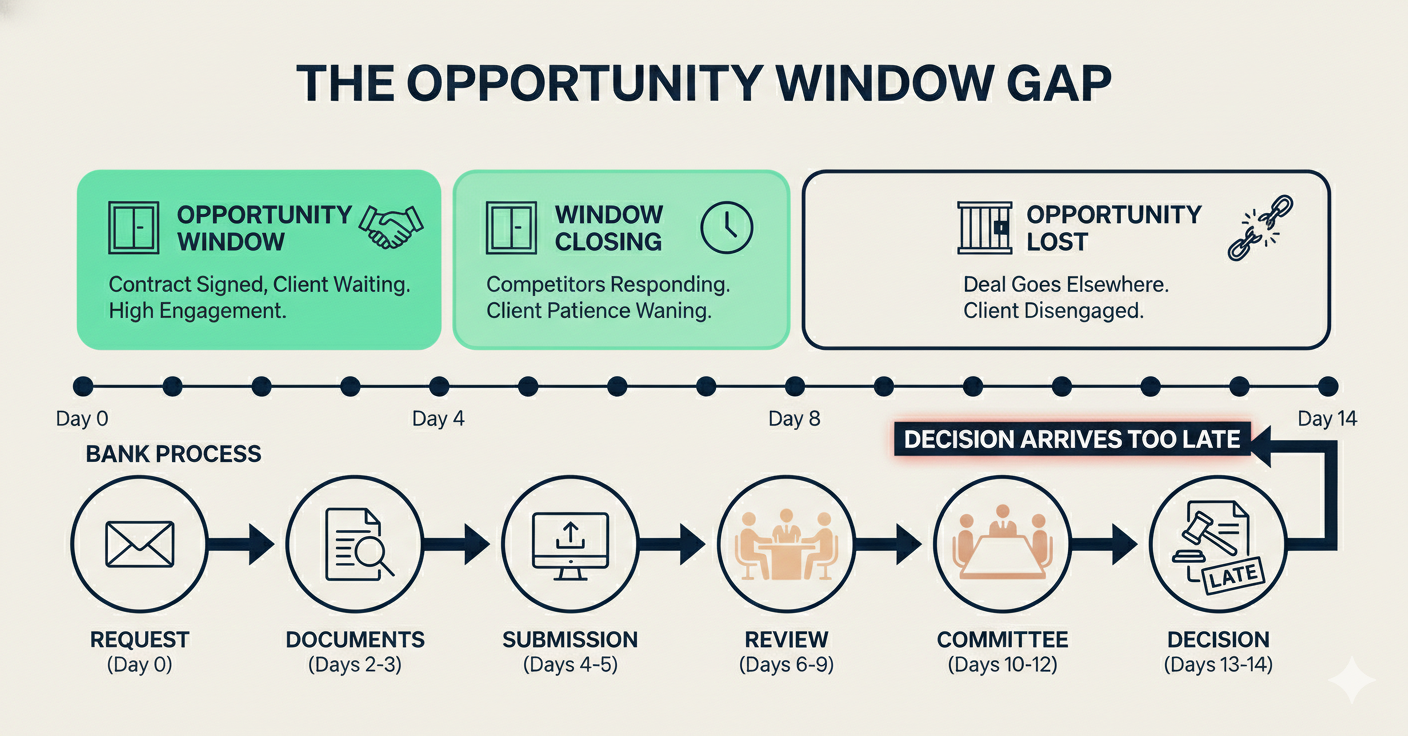

Ahmed runs a logistics company in Dubai. Wednesday morning, 9 AM. He gets confirmation on a $200,000 contract—excellent news, except he needs $80,000 for equipment within 72 hours, and his working capital is tied up in receivables clearing next month.

He calls his relationship manager. Eight-year customer. Perfect payment history. Growing 31% year-over-year.

"I need $80,000 short-term. Can we move quickly?"

"Absolutely. I'll need three years' financials, trade license, receivables report, and the contract copy. Credit committee takes 7-10 days once we submit."

Ahmed hangs up. In ten days, the opportunity is gone.

This scene repeats thousands of times daily across Dubai, Singapore, London, New York.

The bank isn't being difficult. The relationship manager wants to help. The credit team will work diligently. Everyone performs their role correctly.

The system itself fails Ahmed. Not through poor execution, but through architectural design that made sense in 1985 but breaks in 2024.

The Timing Mismatch: Research across 40 markets shows 68% of SME growth opportunities require financial decisions within 5 days. Average bank credit approval: 10-14 days. This isn't a service failure—it's structural misalignment.

II. The Four Eras of Banking Architecture

Banking systems have evolved through distinct eras—not incremental improvements, but fundamental capability shifts that redefined what banks could do:

|

Era |

Core Capability |

Timeframe |

Defining Technology |

Customer Relationship |

|

Era 1: Custodial |

Store value safely |

1800s-1960s |

Vaults, ledgers |

Safekeeping provider |

|

Era 2: Transactional |

Move money efficiently |

1970s-2000s |

ATMs, cards, SWIFT |

Transaction processor |

|

Era 3: Digital |

Access anywhere |

2000s-2020s |

Mobile, cloud, APIs |

Convenience enabler |

|

Era 4: Thinking |

Anticipate needs |

2020s→ |

AI agents, LLMs |

Strategic partner |

Each transition represented new architectural capabilities, not better execution of old ones:

- Era 1→2: ATMs didn't make branches better; they created 24/7 access branches couldn't provide

- Era 2→3: Mobile didn't make ATMs better; it enabled banking anywhere, not just at machines

- Era 3→4: Thinking systems don't make digital better; they enable anticipation, not just access

Here's the pattern most organizations miss:

They're investing billions perfecting Era 3—faster apps, better UX, smoother onboarding—while the market shifts to Era 4. They're optimizing reactive banking when they should be architecting banks that think.

The distinction matters. A bank that thinks doesn't just process requests faster. It observes patterns, reasons about context, anticipates needs, and acts proactively—with permission. Intelligence becomes infrastructure, not feature.

The question senior executives must ask: Are we building better Era 3 capabilities, or architecting for Era 4?

Because those require fundamentally different strategies, systems, and organizational models.

III. What "Reactive Architecture" Actually Means

Reactive banking operates on a fundamental sequence:

Customer Need → Customer Request → Bank Receives →

Gather Information → Analyze → Decide → Communicate

This made perfect sense when architected in the 1970s-1990s:

|

Historical Context |

Why Reactive Was Optimal |

Today's Reality |

|

Information was scarce |

Couldn't anticipate without data |

Data is abundant, real-time |

|

Processing was manual |

Had to wait for trigger |

Can analyze continuously |

|

Communication was slow |

Couldn't reach proactively |

Instant digital channels |

|

Business cycles were quarterly |

Delays were acceptable |

Real-time operations |

|

No alternatives existed |

Customers had no choice |

Expectations set by Amazon, Netflix |

In that environment, reactive architecture was brilliant—even optimal.

Banks couldn't anticipate needs because they lacked real-time data, processing power, communication channels, and customer expectations for proactive service.

But everything changed except banking architecture.

Businesses today operate in real-time. Orders flow through digital marketplaces. Inventory updates instantly. Supply chains shift hourly. Currency rates fluctuate continuously.

Banks, however, still wait for requests, gather documents, analyze historically, and respond days later.

They've digitized the interfaces—mobile apps instead of branches—but the underlying logic remains unchanged: wait, respond, process.

A thinking bank would behave differently. It would observe transaction patterns continuously, reason about emerging needs, and surface relevant solutions before customers recognize them. The same data. Different architecture. Fundamentally different relationship.

IV. The Information Paradox

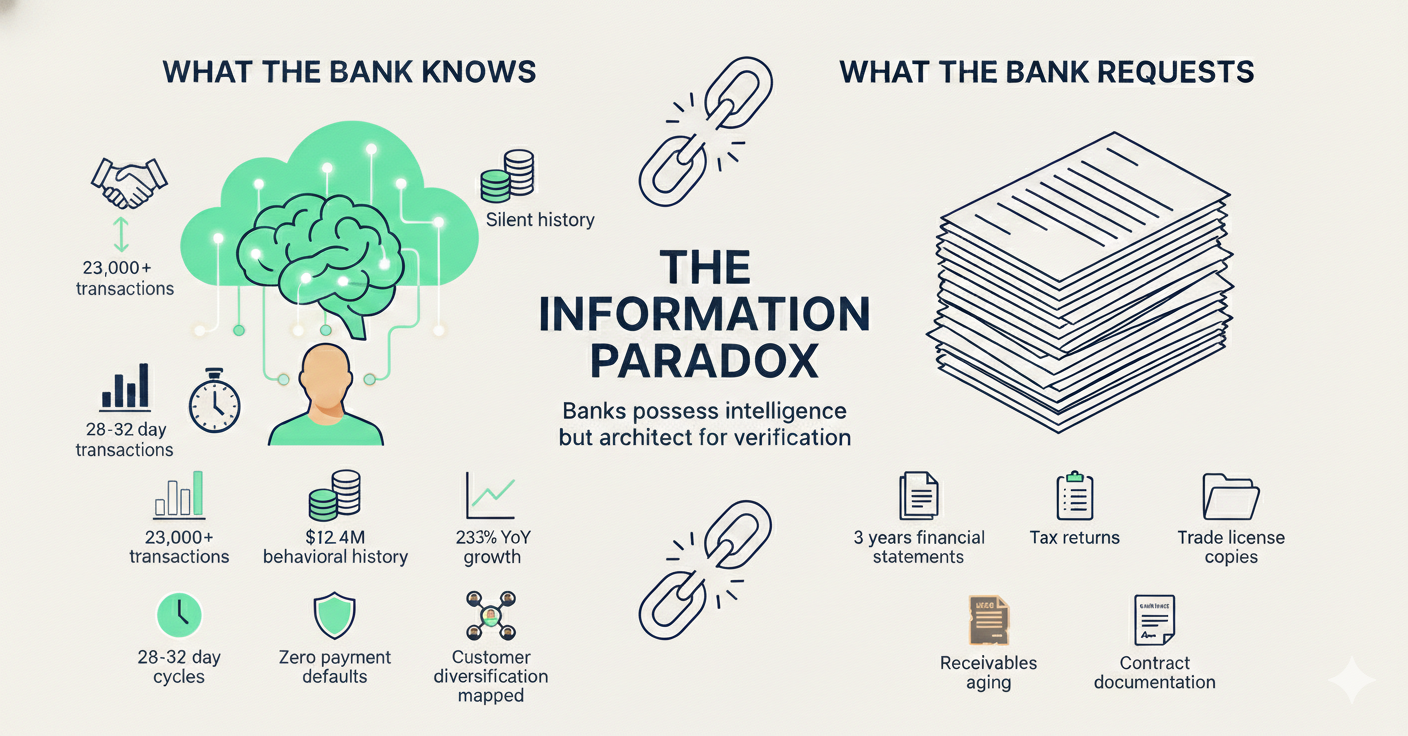

Return to Ahmed for a moment. Over eight years, his bank has processed:

- 23,000+ transactions through his account

- $12.4 million in total volume

- 340+ monthly revenue cycles

- 96 quarterly seasonal patterns

- Perfect payment history on existing facilities

From this behavioral data, the bank's systems know:

✅ Monthly revenue patterns (seasonal peaks Q4, slower summer)

✅ Payment discipline (zero missed payments, healthy balances)

✅ Customer concentration (22% largest client—healthy diversification)

✅ Growth trajectory (31% YoY for three years)

✅ Operational rhythms (payroll, leases, supplier payments)

✅ Cash conversion cycle (28-32 days, predictable)

Yet when Ahmed needs $80,000 for a time-sensitive opportunity, the bank asks him to manually compile and prove what it already knows through data.

This paradox exists because of architectural design, not capability limitations.

Banks are built to analyze static snapshots, not dynamic patterns. A thinking bank would use behavioural patterns to anticipate needs. A reactive bank uses those same patterns only for retrospective verification. The data is identical. The architecture determines whether systems think or simply process.

- Traditional question: "What did this business look like last quarter?"

- Relevant question: "What does 8 years of behavioural data suggest about short-term credit risk?"

The bank possesses data to answer the second question but is architecturally designed only to process the first.

V. The Organizational Dynamic

There's a structural challenge to transformation that rarely gets discussed openly.

Architectural transformation often threatens the expertise of those best positioned to lead it. CIOs who built careers modernizing legacy systems must now advocate for architectures that make that expertise less relevant. COOs whose processes define operational excellence must champion systems that automate those processes. Relationship managers who pride themselves on knowing customers must embrace systems that might know customers better.

This isn't malice. It's rational self-preservation within institutional contexts.

Innovation labs get created—separated from core banking—because integration would disrupt existing power structures. Pilots target non-strategic segments because failure there doesn't threaten core operations. Consultants get hired to "assess readiness" because the assessment period delays difficult decisions.

The pattern repeats across organizations: transformation initiatives that appear to advance architectural change often function to contain it.

This is why challengers have structural advantages. They don't have constituencies to protect, processes to preserve, or expertise to defend. They can architect for Era 4 without navigating Era 3 politics.

The system behaves this way not because organizations lack vision, but because institutions are designed to preserve what made them successful.

VI. The Maturity Model: Where Banks Actually Operate

Not all banks operate at the same level of reactivity. Understanding where your organization sits is critical for strategic planning.

The Reactive-to-Thinking Maturity Model:

|

Level |

Characteristics |

Customer Experience |

Most Banks Here |

|

Level 1: Manual

Reactive |

Branch-based, paper forms |

Slow, high friction |

Traditional banks, emerging markets |

|

Level 2: Digital

Reactive |

Online apps, digital docs |

Faster, convenient |

Most digital banks, neo-banks |

|

Level 3: Intelligent

Reactive |

AI-assisted underwriting |

Quick standard approvals |

Leading fintechs, progressive banks |

|

Level 4: Proactive

Advisory |

Pattern recognition alerts |

Receives relevant nudges |

Pilot programs only |

|

Level 5: Thinking

Partnership |

Continuous intelligence |

Banking at right moment |

Not achieved at scale |

The Level 2-3 Trap:

Most "digital transformation" initiatives move banks from Level 1→2 or 2→3. This creates real improvement—faster processes, better UX, lower costs.

But it doesn't change the fundamental architecture from reactive to anticipatory.

A Level 3 bank still:

- Waits for customer requests

- Analyzes primarily historical data

- Makes decisions on static snapshots

- Requires customers to recognize needs

- Operates on request-response logic

It just does all of this faster with better interfaces.

The leap from Level 3 to Level 5—to banks that truly think—requires architectural rethinking, not incremental improvement.

This is why massive technology investments often yield disappointing strategic returns. Organizations optimize reactive architecture (Level 2→3) when they need to transform to thinking architecture (Level 3→5).

Strategic Question: Are your transformation initiatives moving you from Level 2 to 3 (optimization), or from Level 3 to 5 (transformation)? The investment may be similar. The competitive outcomes are radically different.

VII. The Digital Illusion

It's tempting to think digital banks have solved these issues. They haven't.

Digital banks have improved the interface:

- ✅ Apply through apps (not branches)

- ✅ Upload docs digitally (not photocopied)

- ✅ Get decisions in 5 days (not 10)

But the underlying model remains reactive. They still wait for requests, evaluate historically, and respond to articulated needs.

Consider transformation patterns across industries:

|

Industry |

Digital Evolution (Reactive) |

Architectural Transformation (Anticipatory) |

Banking Status |

|

Retail |

Online catalogs (browse & buy) |

Predictive recommendations (Amazon) |

Still reactive |

|

Transport |

App booking (request & wait) |

Predictive positioning (Uber) |

Still reactive |

|

Entertainment |

Digital libraries (browse) |

AI-curated feeds (Netflix) |

Still reactive |

|

Banking |

Digital access, faster processing |

Thinking partnership |

← We are here |

Banking has digitized the reactive model but hasn't transformed to anticipation.

The Narrative Gap:

There's an industry narrative that digital banks are disrupting traditional banking. The reality is more nuanced. Most digital banks are reactive banking with superior UX. They wait for you to request services, just through prettier apps. Same architecture. Better interface.

This narrative actually benefits traditional banks. If the competitive threat is "better UX," the response is "improve our apps." Significant but manageable.

The real disruption—thinking architecture—hasn't arrived at scale yet. When it does, both traditional banks and current digital banks will face similar challenges. The competitive frame isn't traditional vs. digital. It's reactive vs. anticipatory.

Understanding this distinction matters. Organizations optimizing for the wrong competitive dimension will find themselves well-positioned for yesterday's battle.

VIII. The Backward-Looking Lens

Traditional banking assessment is fundamentally historical. Financial statements show last quarter. Tax returns reflect the previous year. Credit committees review past performance.

This has sound logic: past behavior is the best predictor of future behavior.

In stable environments, this works. But business environments are increasingly dynamic, and historical assessment struggles with transitions.

Consider a real scenario from Dubai:

A software services company had an exceptional 2023—$3.2M revenue, 42% margins, perfect payment history. Financial statements look pristine.

But in January 2024, their largest client (65% of revenue) announced they're moving development in-house. Contract ends March. The company is pitching new clients with promising conversations, but current cash flow is stressed.

Traditional backward assessment:

- ✅ Excellent financial history

- ✅ Strong margins

- ✅ Perfect payment record

- Decision: Approve credit increase

Forward-looking assessment:

- ⚠️ Revenue collapsing in 60 days

- ⚠️ Pipeline uncertain, not confirmed

- ⚠️ High concentration risk materializing

- Decision: Cautious, require new client confirmations

Backward-looking models make suboptimal decisions because they cannot easily incorporate context, trajectory, or emerging patterns not yet visible in historical documents.

A thinking bank would observe the concentration risk developing through transaction patterns, model the revenue impact of client loss, and proactively engage before the crisis point. Same data. Different temporal orientation. Fundamentally different outcome.

The Credit Paradox: Businesses most deserving of credit support are often in transition states that historical analysis penalizes, while businesses approaching stress often look stable in rear-view assessment.

IX. A Moment of Reflection

What makes this transition genuinely difficult isn't technology—the systems exist. It isn't regulation—frameworks are evolving. It isn't even organizational complexity, though that's real.

It's that thinking architecture requires a different kind of institutional humility.

Reactive banking is built on control: customers request, we analyze, we decide, we grant or decline. There's certainty in that model. Clear boundaries. Defined processes. Measurable outcomes. Human judgment sits at the center of every decision.

Thinking architecture requires admitting that static control is no longer enough. That systems observing continuous behavioral patterns might understand customer needs before customers articulate them. That the bank's role shifts from gatekeeper to partner. That intelligence distributed across autonomous agents—with appropriate human oversight—might serve customers better than centralized committees making periodic decisions.

This isn't a technical challenge. It's a philosophical one.

And perhaps that's why transformation proves so difficult—not because organizations can't build the future, but because embracing it means letting go of assumptions that made them successful in the past. The very instincts that drove excellence in Era 3 can become obstacles in Era 4.

Recognizing this isn't weakness. It's the first step toward genuine transformation.

X. Why This Moment Matters: The AI Inflection Point

For decades, reactive architecture was suboptimal but inevitable. Banks adapted. Businesses maintained larger reserves, planned further ahead, accepted delays.

Something fundamental changed in 2023-2024.

Not because business velocity increased (though it did), but because the technical capability to architect thinking systems crossed the feasibility threshold.

Before 2023: AI Could Recognize Patterns

- Fraud detection

- Credit scoring

- Customer segmentation

- Recommendation engines

After 2023: AI Can Reason, Plan, and Act

- Large Language Models with contextual understanding

- Agentic systems that pursue multi-step goals

- Autonomous decision-making with explainability

- Continuous learning from outcomes

This combination—context + reasoning + planning + explainability + learning + autonomy—enables thinking architecture for the first time.

Previous AI: "This customer has 73% probability of needing working capital in 90 days."

Thinking System: "This customer will need $65,000 in approximately 18 days when receivables-payables gap peaks. Based on 8-year payment history and seasonal patterns, I recommend proactively offering 30-day facility at 8.2% APR, aligned to their cash conversion cycle. Here's my reasoning: [detailed explanation]. Here's how I calculated the amount and timing: [transparent methodology]."

The first is prediction. The second is partnership.

The Capability Shift: For the first time in banking history, the technology exists to match system capability with business need velocity. Reactive banking wasn't just a choice—it was a constraint. That constraint has lifted.

We'll explore this technical transformation in depth in Chapter 3. The key insight for now: this isn't "someday" technology. It's deployable today.

The strategic window for positioning is 2024-2026. Organizations that commit to thinking architecture now will build data advantages and learning loops that become nearly impossible for followers to replicate.

XI. The Economics of Architectural Lag

The cost of maintaining reactive architecture while competitors transform isn't theoretical.

Market Dynamics:

- Global SME banking: $850B annual revenue

- Addressable with thinking models: ~$340B (40% of market)

- Premium pricing potential: 15-25% for anticipatory services

Cost of Delayed Transformation:

- Banks at Level 3 face 8-12% annual attrition to Level 4/5 competitors

- Average transformation timeline: 24-36 months

- Each year of delay = 2-3% market share erosion (compounding)

First-Mover Economics:

- Data network effects create 30-40% cost advantages after 24 months

- Customer acquisition: 60% lower costs (inbound vs. outbound)

- Lifetime value: 2.3x higher (partnership vs. transaction)

This mirrors patterns in adjacent transformations. When mobile payments transformed commerce, early movers (Alipay, Paytm, M-Pesa) captured 40-60% market share that late movers couldn't reclaim despite superior resources.

The window is 2024-2026. After that, organizations find themselves explaining to boards why they're multiple years behind competitors who made earlier commitments.

XII. Common Transformation Patterns (And Why They Stall)

Most organizations attempting architectural transformation follow predictable patterns. Understanding these patterns helps avoid them.

The Innovation Quarantine: Creating separate innovation labs disconnected from core banking signals transformation as experimental rather than strategic. These labs produce interesting pilots that rarely integrate into actual operations.

The Assessment Loop: Hiring consultants to evaluate readiness for 6-12 months while competitors build and learn. Assessment becomes a comfortable alternative to commitment.

The Safe Pilot: Testing with non-strategic customer segments to "prove the concept" while protecting core operations. Mediocre results from low-stakes pilots then justify cautious approaches.

The ROI Trap: Requiring traditional ROI justification for architectural transformation. The right question isn't incremental return—it's strategic positioning for an inevitable market shift.

The Capacity Staffing: Assigning people with availability rather than best talent. This signals transformation as secondary priority and produces secondary results.

The Feature Addition: Maintaining reactive architecture while adding "AI features." This optimizes the old model rather than building the new one.

These patterns emerge not from lack of vision but from institutional dynamics that make containment safer than transformation.

Organizations that successfully transform do precisely none of these things. They integrate transformation into core operations, commit before perfect clarity emerges, staff with A-players, and architect for Era 4 rather than optimizing Era 3.

The difference isn't resources or capability. It's commitment.

XIII. Two Futures, 2030

FUTURE A: You Transformed (Committed 2024-2026)

Your bank operates at Level 5—thinking partnership. You serve 3x more SMEs with 40% fewer staff. NPS: 72 vs. industry 31. Customer acquisition cost: $180 vs. industry $640. You're the category leader. Fintechs study your model.

Your 2024 commitment to thinking architecture—despite skepticism and organizational resistance—created compounding advantages competitors couldn't overcome. Data network effects improved continuously. Learning loops enhanced models daily. Customers experienced partnership, not transaction processing.

FUTURE B: You Optimized (Continued Era 3, 2024-2026)

Your bank operates at Level 3.5—excellent reactive banking. You've lost 30% market share to thinking competitors. Cost-to-serve: 2.3x theirs. You're attempting "catch-up transformation" your board questions: "We already spent $200M on digital transformation."

Your 2024 decision to optimize reactive banking—safer, more defensible—locked in structural disadvantage. You perfected Era 3 while competitors architected Era 4.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Which future do you want? More importantly: which are your current decisions actually creating?

They're rarely the same answer. And that gap is where strategic positioning happens—or fails to happen.

XIV. The Strategic Imperative

This chapter has mapped the reactive banking paradigm: what it is, why it developed, and why it no longer serves modern business velocity.

We've established:

✓ Reactive architecture was optimal for its era but is now structurally misaligned

✓ Digital transformation optimizes reactive processes without transforming reactive logic

✓ We're at the transition between Era 3 (digital) and Era 4 (thinking)

✓ AI capabilities crossed the feasibility threshold for thinking systems in 2023-2024

✓ The strategic window for positioning is 2024-2026

The diagnosis is clear: reactive banking is architecturally misaligned with business reality.

But diagnosis without direction is just expensive insight. Senior executives must ask:

For Your Organization:

📊 Where do you sit on the maturity model? (Level 2? 3? Beginning to move toward 4?)

🎯 What's your architectural strategy? (Optimizing reactive or building thinking systems?)

⏰ What's your timeline? (When will you commit? How long will transformation require?)

💰 What's the cost of waiting? (Can you fast-follow, or do first-movers capture insurmountable advantages?)

🔮 Do you have architectural foundation? (Real-time data infrastructure? AI capabilities? Organizational readiness?)

The reality organizations face:

Waiting for "proof" before committing means entering transformation when early movers have built insurmountable data advantages. The gap from Level 3 to Level 5 won't be closeable through incremental improvement.

Transformation to thinking architecture requires:

- Complete system redesign

- New data infrastructure

- Different organizational models

- Transformed talent requirements

- Cultural reinvention

- 24-36 months minimum

Organizations starting in 2026 will compete against organizations that started in 2024—with two years of learning, data network effects, and customer relationships already compounding.

The Strategic Window: First-movers in thinking architecture will build compounding advantages through data network effects and learning loops. The window for positioning is 2024-2026. By 2027-2028, thinking capabilities become table stakes, and late movers face structural disadvantages.

This isn't speculative future. This is strategic present.

The chapters ahead explore what it means to architect banks that think—not as metaphor, but as design philosophy. Systems that observe patterns, reason about context, anticipate needs, and act with permission. Intelligence as infrastructure, not feature.

But transformation begins with recognizing that the question isn't whether banking will evolve from reactive to thinking architecture.

The question is who positions for that evolution now, and who explains to stakeholders in 2027 why they're three years behind.

Key Takeaways

For Bank CEOs:

- Reactive architecture isn't an execution problem—it's structural obsolescence

- Digital transformation maintaining reactive logic is optimization, not transformation

- The strategic question is timing: commit to thinking architecture now or explain delays later

- First-movers capture disproportionate advantages through data network effects

For Chief Strategy Officers:

- The Four Eras framework shows we're at paradigm transition, not incremental evolution

- The maturity model diagnoses current position and required transformation trajectory

- Competitive advantage goes to organizations committing to Era 4 in 2024-2025

- Cost of waiting compounds—each year of delay creates 2-3% market share erosion

For Chief Technology Officers:

- Moving Level 2→3 (better reactive) vs. Level 3→5 (thinking architecture) require fundamentally different approaches

- AI capabilities crossed feasibility thresholds in 2023-2024; technical constraints have lifted

- Intelligence infrastructure creates moats through learning loops that can't be quickly replicated

- The question isn't whether to architect for thinking systems, but whether you start now

For Fintech Founders:

- Reactive architecture creates systematic opening for thinking architecture challengers

- Incumbent advantages (data, relationships) can be overcome through superior architecture

- Technical capability exists today to build thinking systems incumbents can't quickly replicate

- Window for challenger positioning is open but closing as progressive incumbents transform

Further Reading

- "The Innovator's Dilemma" by Clayton Christensen - Why well-managed companies fail at architectural shifts

- "The Coming Wave" by Mustafa Suleyman - Understanding the AI inflection point

- World Bank SME Finance Report 2024 - Documents the $5.7T SME financing gap

- Anthropic Research on Constitutional AI - Technical depth on explainable agent systems

Join the Conversation

Where does your organization sit on the maturity model? What's preventing movement toward thinking architecture—technology, organization, strategy, or institutional dynamics?

Next in Series: Chapter 2 - From Storing to Thinking

We'll trace banking's architectural evolution and explore what defines genuine paradigm shifts versus incremental improvements. If reactive banking is Era 3, what does Era 4—banks that truly think—actually look like, and how do organizations build toward it?

About This Series

The Thinking SME Bank explores banking's transformation from reactive systems to intelligent partners. Written for senior executives, fintech leaders, and strategic consultants navigating the shift from digital optimization to intelligent anticipation.

Word Count: 4,520 words